Stamp duty in 2026: Rates, changes and everything UK buyers need to know

Discover the latest Stamp Duty rates, tax rules, and smart strategies for UK home movers. Our guide helps you plan your next property purchase and avoid costly surprises.

10 mins read

25-06-2026

Similar Guides

More guides arriving soon!

Moving home is exciting, but let's be honest, the costs can make your wallet weep. One of the biggest expenses you'll face as a buyer is Stamp Duty Land Tax (SDLT). Don't worry, though, we're here to break it all down, so you know exactly what you're dealing with.

Think of this as your friendly guide through the stamp duty maze. We'll cover everything from how much you'll pay, to clever ways you might save a few quid. No jargon, no confusing legal speak, just the facts you need to budget appropriately for your home purchase.

What is Stamp Duty Land Tax (SDLT)?

Stamp duty is a tax you pay to the government when you buy a property in England or Northern Ireland. It's calculated as a percentage of your property's purchase price, and yes, it can add up to quite a chunk of change.

The good news? Not everyone pays the same rate, and some handy exemptions might help reduce your bill. The amount you pay depends on several factors, including the property price, whether you're a first-time buyer, and whether you already own another property.

Stamp Duty is one of several significant costs to budget for when buying a property. For a full breakdown of every fee involved, see our guide to the hidden costs of buying a house.

2026 Stamp Duty rates and thresholds

Standard residential property rates

Here's how the current Stamp Duty bands work for most home buyers:

Property prices | SDLT |

|---|---|

up to £125,000 | 0% (that's right, nothing to pay!) |

£125,001 to £250,000 | 2% |

£250,001 to £925,000 | 5% |

£925,001 to £1.5 million | 10% |

over £1.5 million | 12% |

The clever bit is that you only pay the higher rate on the portion of the price that falls into each band, not the entire purchase price.

First-time buyer relief

First-time buyers get a helping hand with reduced rates:

- £0 to £300,000: 0% (even better than the standard rate!)

- £300,001 to £500,000: 5%

This relief applies to properties up to £500,000. If the property price is over £500,000 you can’t claim the relief, and you will need to follow the rules for standard buyers. When buying a property over £500,000, then you'll pay the standard rates on the amount above the £500,000.

New to buying? Our first-time buyer guide covers deposits, mortgages and everything else you need to know.

Additional property surcharge

Already own a property? You'll face an additional 5% surcharge on top of the standard rates for any additional properties. This applies to second homes, buy-to-let investments, and holiday homes.

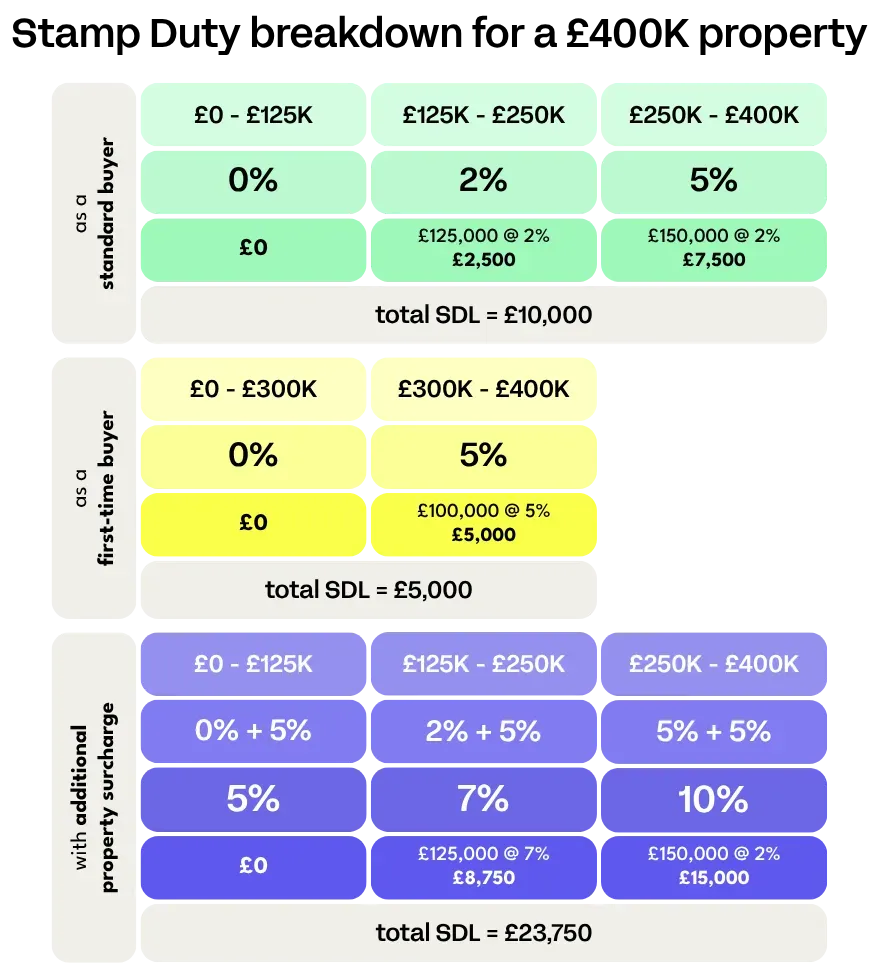

How to calculate your Stamp Duty bill

Let's work through a real example to make this crystal clear.

If you're buying a property worth £400,000, you'll pay:

- £10,000 on Stamp Duty Land Tax as a standard buyer.

- as a first-time buyer that bill goes down to £5,000. Pretty significant difference, right? This is why understanding your eligibility for reliefs is so important.

- £23,750 as a second home or additional property.

You can also use the official HMRC stamp duty calculator to get an exact figure for your purchase price.

Who qualifies as a first-time buyer (FTB)?

To qualify for first-time buyer relief, you must:

- Have never owned a property anywhere in the world.

- Be buying a property worth £500,000 or less.

- Intend to live in the property as your main residence.

If you're buying with a partner, both of you must be first-time buyers to qualify for the relief. If one of you has owned property before, you'll pay the standard rates for Stamp Duty. You can check the full first-time buyer relief criteria on GOV.UK.

Stamp Duty exemptions and reliefs

Properties under £125,000: Any residential property costing £125,000 or less is completely exempt from stamp duty. This makes smaller properties and many regional homes particularly attractive for budget-conscious buyers.

Shared ownership schemes: If you're buying through a shared ownership scheme, you only pay stamp duty on the portion you're purchasing, not the full market value. You can also elect to pay stamp duty on the full market value upfront to avoid paying more later when you "staircase" (buy additional shares).

Transfers between spouses: Transferring property between married couples or civil partners is generally exempt from stamp duty, if it’s done as part of a formal, written divorce or separation agreement signed by both, or following a court order because you’re divorcing or dissolving a civil partnership — provided there are no other buyers involved.

When and how to pay Stamp Duty

You've got 14 days from the completion date to file your Stamp Duty return and pay the tax. Miss this deadline, and you'll face penalties and interest charges — not exactly the housewarming gift you want.

Your solicitor or conveyancer will typically handle this for you as part of the purchase process. They'll calculate the amount due, complete the necessary paperwork, and ensure payment reaches HMRC on time. For full details on filing and payment, see the HMRC guidance on Stamp Duty Land Tax.

Not sure what your conveyancer does? Read our guide on how long conveyancing takes and what's involved.

Regional differences in Stamp Duty

Scotland: Land and buildings transaction tax (LBTT)

Scotland has its own property tax system called Land and Buildings Transaction Tax, with different rates and thresholds to England and Northern Ireland:

Property price | LBTT | |

|---|---|---|

£0 to £145,000 | 0% | |

£145,001 to £250,000 | 2% | |

£250,001 to £325,000 | 5% | |

£325,001 to £750,000 | 10% | |

over £750,000 | 12% |

First-time buyers in Scotland don't pay LBTT on properties up to £175,000. The remainder is exactly the same as a standard purchase.

Buyers purchasing a second or additional property pay an Additional Dwelling Supplement (ADS), applied at 8% of the total purchase price — this is paid in addition to any LBTT. Properties under £40,000 are not subject to ADS.

Wales: Land Transaction Tax

Wales operates its own system called Land Transaction Tax, administered by the Welsh Revenue Authority. There's no first-time buyer relief available in Wales.:

Property price | Standard LTT | Property price | Multiple Dwellings LTT |

|---|---|---|---|

£0 to £225,000 | 0% | £0 to £180,000 | 5% |

£225,001 to £400,000 | 6% | £180,001 to £250,000 | 8.5% |

£400,001 to £750,000 | 7.5% | £250,001 to £400,000 | 10% |

£750,001 to £1.5 million | 10% | £400,001 to £750,000 | 12.5% |

over £1.5 million | 12% | £750,001 to £1.5 million | 15% |

over £1.5 million | 17% |

Smart ways to reduce your Stamp Duty bill

Time your purchase strategically

Keep an eye on government announcements. Temporary reliefs and threshold changes do happen and timing your purchase around these can save thousands.

Consider property price negotiations

If you're close to a stamp duty threshold, negotiating the price down even slightly can sometimes drop you into a lower band, saving more than the reduction in purchase price.

Separate land and property purchases

In some cases, particularly for new builds, you might be able to purchase the land and property separately to optimise your stamp duty position. This is complex territory though, worth discussing with your solicitor.

Chattels and fixtures

If the seller has left items such as carpets, curtains, ovens or furniture behind, make sure the cost of these fixtures and fittings haven’t been factored into the property price. This only makes your stamp duty bill higher. Offer to pay for these items separately so they’re not taxable. Again, professional advice is essential here as HMRC might think you’re taking things too far.

Common Stamp Duty mistakes to avoid

Missing the 14-day deadline: This is the big one. Late filing means penalties starting at £100, plus daily charges and interest. Your solicitor should handle this, but it's worth keeping an eye on the timeline.

Incorrectly claiming first-time buyer relief: HMRC takes a dim view of false claims. Make sure you genuinely qualify before claiming any reliefs, the penalties for getting it wrong are severe.

Forgetting about additional properties: If you own any property anywhere in the world, you'll likely face the additional property surcharge. This includes inherited properties you might have forgotten about.

Not considering future plans: Buying a property you plan to rent out immediately? You'll pay the additional property surcharge even if it's your first purchase. Think about your intentions carefully.

If you're buying in a chain, read our guide to buying a house in a chain to understand how completion timelines work.

Stamp Duty and new build properties

New build properties follow the same stamp duty rules, but there are a few extra considerations:

- Help to Buy schemes: These can affect your stamp duty calculation.

- Shared ownership: You might pay stamp duty differently depending on your purchase structure.

- Off-plan purchases: The stamp duty is based on the final purchase price, not any deposit paid during construction.

Planning your moving budget

Stamp duty should be a key part of your moving budget calculations. Here's what else to factor in:

- Legal fees: Typically £1,000-£2,000 — get multiple quotes to compare costs.

- Survey costs: £300-£1,500 depending on the type of survey — find out the cost.

- Removal costs: Compare firms and costs to find the best deal.

- Home insurance: Required to exchange contracts.

- Emergency fund: Always good to have a buffer for unexpected costs.

Remember, Stamp Duty is paid on completion, so you’ll need this money available alongside your deposit and other moving costs.

For a full breakdown, see our guide to the hidden costs of buying a house.

Making Stamp Duty work for your move

Understanding Stamp Duty doesn't have to be a headache. Armed with the right information, you can budget accurately and maybe even find ways to reduce your bill legally. The key is getting professional advice tailored to your specific situation. Every property purchase is different, and what works for your mate down the pub might not work for you.

Remember, while Stamp Duty is a significant cost, it shouldn't be the only factor in your property decision. Focus on finding the right home for your needs and budget, then factor in all the associated costs, including stamp duty, to make sure everything adds up.

In a nutshell

Moving house is a big step, but with the right preparation and understanding of costs, you'll be well-equipped to make confident decisions. After all, knowledge is power, and in this case, it might just save you some serious money too.